Paul Krugman raises a puzzle:

[C]orporations are taking a much bigger slice of total income — and are showing little inclination either to redistribute that slice back to investors or to invest it in new equipment, software, etc.. Instead, they’re accumulating piles of cash.Tyler Cowen thinks there is no puzzle:

If there is a problem, it is because no one sees especially attractive investment opportunities in great quantity...That’s a problem at varying levels of corporate profits and some call it The Great Stagnation.But I'm not satisfied with this answer. If there is a Great Stagnation, and corporations see no attractive opportunities for growth, then shouldn't they just return their earnings to shareholders as dividends?

Standard corporate finance theory says that companies try to generate returns for shareholders in one of two ways. Either 1) the company reinvests its earnings in the business (i.e. "business investment"), raising the company's value and allowing shareholders to reap a capital gain, or 2) it pays its earnings to shareholders as dividends. Now, since the 1990s, we've gotten used to thinking of companies as rarely paying dividends. But the reason for that was that there were (or at least, companies thought there were) many important growth opportunities to be had; companies took their earnings and reinvested them.

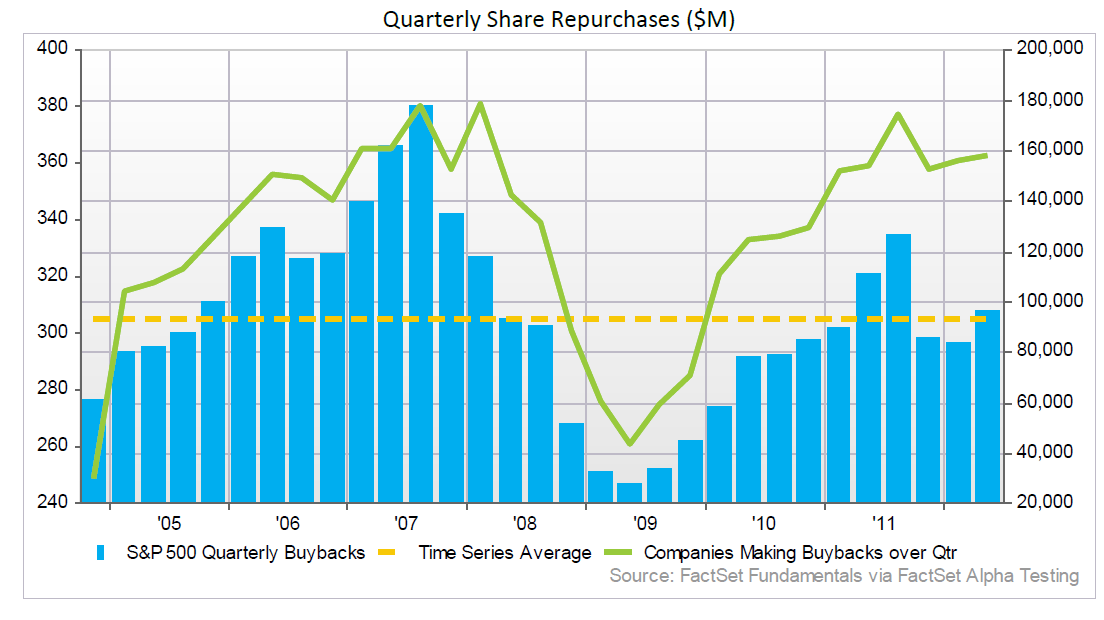

But now, U.S. companies are taking their earnings and holding them in short-term marketable securities ("cash"). That money is not being reinvested in the businesses. And it's not getting handed back to the shareholders as dividends; in fact, dividend payout rations and dividend yields are both at historic lows. (Share buybacks are reasonably strong, though that still doesn't explain the cash hoards, especially with interest rates so low.)

{kind=link}

{kind=link}

If companies saw a Great Stagnation coming, you'd expect them to be giving shareholders their money. But they're not. Why?

I'm not much of a corporate finance guy, so I'm not up on the literature on questions like this. But a few possible explanations could be: 1) corporations want to invest, and just haven't decided what to invest in yet. Uncertainly about the Chinese economy, the European economy, new technology, etc. means that corporations think there will be good growth opportunities but as yet have no firm idea of what those opportunities will be. 2) The link between management and shareholders has totally broken down. Management is acting in their own interests instead of shareholders', and shareholders haven't really noticed this, possibly because dividends were so low in the 1990s and 2000s. 3) Companies do intend to pay some big dividends, but they expect an imminent decrease in the dividend tax rate, so they're sitting on cash for a year or two while they wait for that. 4) Companies are holding the cash as insurance against a possible imminent calamity, such as a new financial crisis, in which they will need lots of liquidity.

Anyway, answering this puzzle is a task for corporate finance researchers. But I think that there is clearly a puzzle here. A lack of good investment opportunities, or a Great Stagnation, is not enough to explain the patterns we are seeing.

(And yes, I realize that this "puzzle" is really just the question of why corporations hold large cash balances at all. But in the current environment, with cash holdings at very high levels, it's an even more salient question than usual.)

Update: Tim Taylor flags some interesting research on the subject. It turns out that the trend toward holding more cash started in the 90s. Also, the paper Taylor cites mentions another reason for holding cash, which I forgot: repatriation tax avoidance. The tax dodge explanation rings true to me, whatever other factors are also present. This means we could induce companies to hold less cash by cutting corporate tax rates.

Tidak ada komentar:

Posting Komentar